Home Cost Averaging

Home cost averaging is a term I use to describe lowering the cost of building a real estate portfolio that is similar to dollar cost averaging. The key takeaway is not to wait for the perfect time to invest in real estate, but rather to regularly and routinely find deals where the numbers work. Time in the market will typically beat market timing given enough time and trends toward the upside.

There are two things that typically make one successful in real estate investing - investing early and avoiding bankruptcy. Usually, real estate investors use mortgages or other loans to buy real estate and finance the cost of repairs and upgrades. This debt means that the real estate investor is leveraged and this “turbocharges” the possible gains and losses. The challenge for real estate investors in the US is to find enough deals early enough in life that they have enough time to appreciate (through real appreciation driven by supply and demand and through nominal inflation) while the costs are lower than the cashflow and the investor remains solvent (the mortgage rate is locked and the other costs of maintaining and managing the property are lower than the cashflow and/or ability to pull equity out of the appreciation for major expenses). Home cost averaging reduces the risk of market timing and waiting too long for the right time to invest.

A common refrain from successful real estate investors is that they are always buying real estate - whether real estate is cheap or expensive. Barbara Corcoran has frequently said that she overpays for real estate all the time. This common strategy among successful real estate investors is something I like to call “home cost averaging.” When real estate is cheap (such as when the housing market is bottoming in 2012 after the 2008 housing crisis) you can buy more investment properties. When real estate is expensive (more recently), it’s harder to find a deal where the cashflow numbers work so you end up buying less real estate. Given that US housing is currently undersupplied, population is expected to continue to grow, lumber and sand supplies needed for framing, concrete, and other construction materials are expected to become more scarce, and given historical inflation and the Fed’s target rate of 2% inflation, most real estate investors expect the price of homes to be more expensive in the long term (say 30 years from now) and thus are willing to always buy real estate now to generate long term returns and wealth.

A way to get started, is by jumping on the housing ladder as soon in life as possible. I call this investing before nesting. You want property growth before the oath. Your first home doesn’t need to be your dream home, and you don’t need to live in the home with a significant other or family. The easiest way to afford a home and get on the property ladder is by getting roommates after the purchase. This can reduce your mortgage to lower than the rent you would otherwise pay, and sometimes the rents you collect from roommates can even be more than your mortgage and expenses and you can cashflow the property. This is often called house hacking when you create cashflow out of your primary residence. You can even buy a multifamily property (up to 4 units with a Fannie loan), live in one, and use the expected rents of the other units as income to qualify for the loan. You can even do this with a first time homebuyer’s mortgage where the down payment amount can be a lower amount than a conventional mortgage. The minimum down payment amount you need to get started can be anywhere from 0% to 5% of the loan.

Building a Real Estate Portfolio, One Property at a Time

If you house hack one house per year, you can build a real estate portfolio of 10 houses in 10 years - all with Fannie loans. When prices are high, you will likely buy less house (less square footage or fewer units or rooms). When prices are low, you will buy more house (more square footage or more units or more rooms). Some mortgages require you to live in the home at least one year as your primary residence before you can convert the home into a rental while other loans may require you to live in the home for two years. This isn’t the quickest way to build a ten property portfolio, but it is one way that can work. I have seen some people speed up their ability to finance each consecutive property by taking their equity out from one property that has appreciated and using it as a down payment on the next property.

It should be said, though, that it is not a given that real estate will always appreciate in real or even nominal terms. When homes become unaffordable for the local people who want to live there, demand (and thus prices) can decline, and that the old adage is usually true that real estate is local - it is usually tied to fundamentals of jobs and wages in the local economy (remote work can disrupt some but not all of those fundamentals). The most important parts of investing in real estate is whether the local population is growing, whether local jobs are expected to grow, and buying at a great price. Investors who buy the wrong deals can go bankrupt, especially if they over-leverage themselves.

To better understand home cost averaging, let’s break down the principle of dollar cost averaging and show how it can lower the average price you pay over time and how it can reduce risk.

Dollar Cost Averaging

The benefits of Dollar cost averaging over market timing are important to understand. When the markets crashed in 2008 and stocks indexes lost more than half of their value , it was easy for many professional investors to recommend investing and going overweight in stocks. The thinking was ‘what do you have to lose? If it all crashes to 0, then we’re going to have bigger problems anyways.’ Still, many others warned against investing at what would be one of the best times to invest in a business cycle (so long as the stocks you picked didn’t go bankrupt or so long as you diversified into index funds). When there’s blood in the streets, that’s when you can find deals. Warren Buffett says “be fearful when others are greedy and greedy when others are fearful.” The problem, though, is you don’t often know how low investments can go, whether individual stocks will go out of business, and you don’t want to need cash waiting for the market to turn around. This is why long term investors caution against “catching a falling knife” and will frequently say that “markets can remain irrational longer than you can remain solvent” (a quote often attributed to John Maynard Keynes). Some then resolve to a strategy of “buy the dip”. The problem is knowing what is a dip and what is a crash. Many stock market crashes also have what’s known as a “sucker rally” or a “bull trap” where all indications seem to show that the market is bottoming out and turning towards the upside; this happens right before the next crash. Some investors will resolve this problem with the strategy of “don’t fight the Fed.” This means that when the Federal Reserve is being hawkish and combating inflation to reach their mandated target of 2%, they will raise interest rates which will increase the cost of borrowing for businesses and lower the price of bonds. Why would I pay the par/face value of a bond at 2% when the Fed is raising interest rates and I can get a higher rate on a “risk free” 10 year treasury note (risk free is in quotations because it is commonly considered an instrument for a risk free rate of return though all investments carry risk)? Stocks can suffer, too, from a hawkish Fed. Some stocks might go out of business if their business is interest rate sensitive (lending companies that rely on refinancing for their business) and more investment dollars may be pulled out of riskier stocks (lowering the price) and put towards less risky bonds (note that there are bonds of all risk levels but US treasuries are considered less risky than stocks in general and AAA rated corporate bonds are often considered less risky than their stock counterparts). The main reason for market timing leading to worse outcomes than dollar cost averaging, though, is psychological. Investors stay too conservative for too long waiting for the right time to buy and wait too long for the right time to sell. It’s not enough to buy at the right time when market timing, you also have to be right a second time when selling unless you hold your investments long term. It should be noted that Fidelity Investments did a study and found that people who forgot about their 401k performed better than those who actively managed it. Warren Buffett also frequently points out that professional investment managers perform worse than a coin flip when comparing their returns minus fees against the S&P 500. He even once said that he had instructed his wife to put all of her money into the S&P 500 in the event of his death.

Dollar cost averaging, on the other hand is a way of circumventing the risks and dangers of market timing. Instead of trying to buy or sell at the right time, you buy (or sell) regularly. The most common implementation of this strategy is investing a set amount each pay period into a 401k, retirement, or brokerage account. By investing regularly, you buy more shares of investments when prices are low and less shares of investments when prices are high. This lowers the average price you pay for your investments compared to what the average price of those same investments were over the same time period. While the difference in price may seem small, given enough time, the returns compound.

Here we see that the rolling average price per share vs the rolling average price paid per share when investing $100 into a security every month. The price you pay is lower than the average price. Dollar cost averaging lowers the price you pay lower than the average price because you buy more shares when prices are low and fewer shares when prices are high.

Looking at the full 10 months below we see that not only do you pay a significantly lower average share price, but there were only 3 months when the price was lower than the average price paid when dollar cost averaging.

It’s worth noting that this shouldn’t suggest if you win the lottery or have some other large lump sum windfall that you shouldn’t invest the money straight away instead of holding money back to invest over several or many years. In our example if you had tried to invest $1000 as a lump sum into this security in 7 of the 10 months, you would have paid a higher price than if you had dollar cost averaged. There were only 3 months out of 10 when a lump sum investment would have been lower than the average price you paid by dollar cost averaging. While this is a rudimentary illustration, it shows that dollar cost averaging can lower the average price you pay for investments and it can sometimes lower the price you would pay lower than a lump sum investment would have.

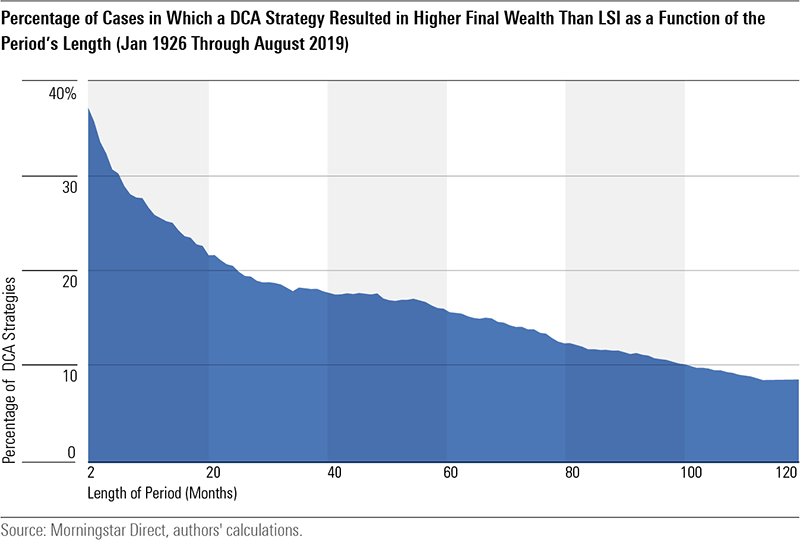

So when does lump sum investing beat out dollar cost averaging? Maciej Kowara and Paul Kaplan from Morningstar wrote a paper “Dollar Cost Averaging: Truth and Fiction” and showed that lump sum investing can beat out dollar cost averaging, especially when given enough time and given a rising market (volatility to the upside). When there is volatility to the downside, dollar cost averaging wins (1). However, this does not suggest one should save money and try to time the market. In fact what it shows is that time in market typically beats market timing over the long term. Dollar cost averaging reduces risk over the short term and during periods of downside volatility, though there are other ways of reducing risk with diversification as Kowara and Kaplan illustrate. Most importantly, as income comes in one should invest it in a suitable manner for their goals as opposed to timing the market.

Above, Kowara and Kaplan show when dollar cost averaging is likelier to beat lump sum investing - in the short run of a volatile market (1).

Above, Kowara and Kaplan show a period of high volatility from 2000 to 2009 when dollar cost averaging would have beaten the performance of the S&P 500. During 2001, 2002, and 2003, dollar cost averaging into the S&P 500 beats a lump sum investment into the S&P 500. During these same years, dollar cost averaging into a diversified portolio of stocks and bonds beats the performance of just stocks (trading the S&P 500) and dollar cost averaging into stocks (1).

Above, Kowara and Kaplan illustrate that dollar cost averaging performs better during periods of significant downside volatility, though time in the market here wins over this longer time period (1).

Above, Kowara and Kaplan show a time period where dollar cost averaging into a diversified portfolio of stocks and bonds beats the S&P 500 during a couple of short time periods, but a lump sum invested in a diversified portolio of stocks and bonds beat the portolio of just stocks during the 70s (1).

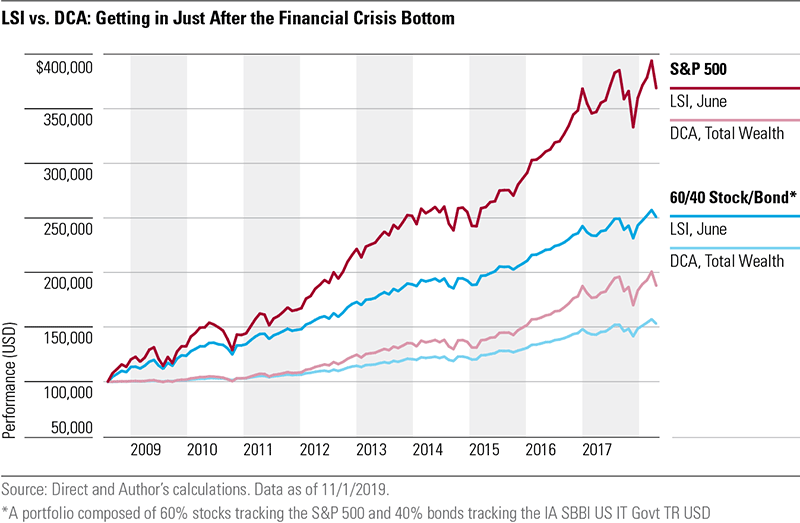

Above, Kowara and Kaplan show that dollar cost averaging from the bottom of the 2008 financial crisis would have produced significantly lower returns than lump sum investing, but this assumes you had some windfall at the bottom of the market in 2008. If you had $100,000 that you saved in cash over a period of time prior to 2008, you may have had inflation eating away at the purchasing power of that money over time. Time in the market often beats market timing in an upward trending market over the long term (1).

Lump Sum Real Estate Investing

There are times when investing in real estate all at once, or over a short period of time, will produce higher returns than regular and routine investing. Given enough time and/or trends toward higher home prices, investing a windfall in real estate or accumulating a lot of properties in a short amount of time through a BRRRR (buy, rehab, rent, refinance, repeat) or seller financing, for instance, can lead to higher returns. A BRRRR allows you to reuse the same down payment money to build your portfolio, though it may cost you time (and the opportunity cost of your time) and seller financing allows you to sometimes pay no down payment.

The problem with both of these strategies is that they often times require more analysis and negotiating and the right market for them to work than a person has the time, knowledge, and ability for and the right accessibility to. A BRRRR can be stopped dead in its tracks and a person can quickly become insolvent if their home values and rents fall. If you are overleveraged, you might be forced to declare bankruptcy, and if you have recourse loans (some DSCR loans are recourse loans), your lender can go after your personal assets. Fannie and Freddie loans are non-recourse, meaning you can hand the keys to them if you default on the loan, though it can impact your credit rating for up to 7 or 10 years. Fannie and Freddie loans may have stricter qualifying requirements than some other types of loans (DSCR loans for instance) and the maximum number of financed properties is capped for Fannie Mae at 10 properties. Freddie Mac limits you to 4 properties, so you may need to find the right lender to accumulate more properties.

Home Cost Averaging Can Reduce Risk and Lower Average Prices Paid

Home cost averaging can reduce the risk of overpaying for the properties in your portfolio by lowering the average price you pay over time compared to the average price of those same properties over time. It does this because you buy more square footage or units or rooms when prices are low and less square footage or units or rooms when prices are high. Home cost averaging performs best when there is downside volatility, and it can build a habit of investing regularly and routinely instead of attempting to wait for the right time to invest. In real estate, the adage is often true that the best time to buy real estate is 10 years ago, and the second best time to buy is today.

About the Author

Cash LeBrun has worked for fintech companies and financial firms for over 13 years of his career in technology and financial services. He received a B.A. in Economics from the University of New Mexico.

Sources Cited:

(1) https://www.morningstar.ca/ca/news/197440/dollar-cost-averaging-vs-lump-sum-investing.aspx

Disclaimer

I am not a financial advisor, attorney, or accountant nor am I holding myself out to be. The contents on this website are for educational purposes only and represent my personal opinions. The information contained on this website is not a substitute for financial advice from a professional who is aware of the facts and circumstances of your individual situation. To make the best financial decision for your needs, you must conduct your own research and seek the advice of a professional with the appropriate licenses if necessary. All investments involve some form of risk and there is no guarantee that you will be successful in making, saving, or investing money; nor is there any guarantee that you won't experience any loss when investing. It is also important to note that past performance does not predict future performance, and any historical analysis does not predict what will happen in the future.